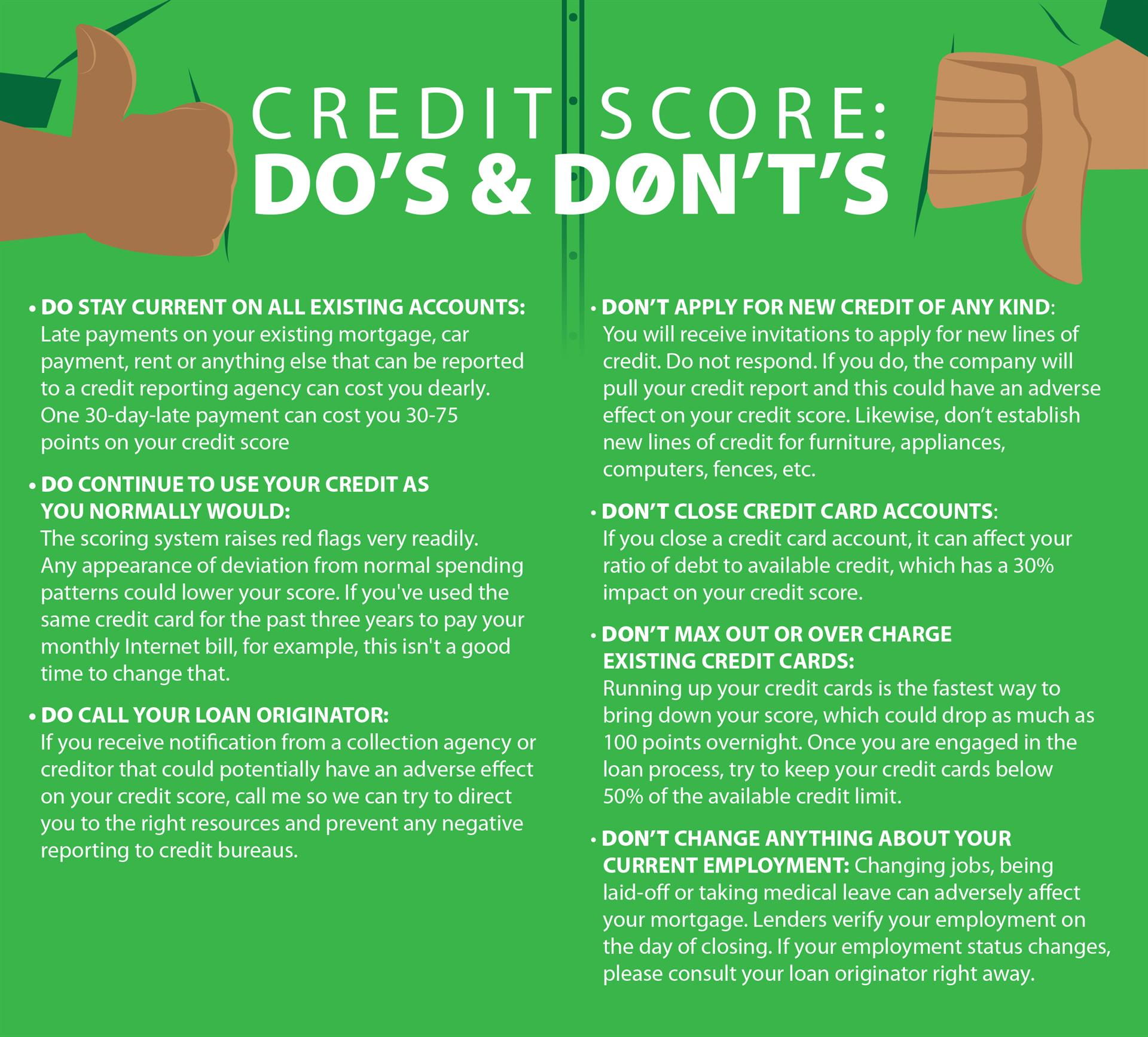

Your credit scores usually determine the price you pay for your money (your mortgages, your auto loans and leases, your credit cards, business loans, etc.).

Perhaps the most significant part of your credit report is your credit score.

Credit scores range from 350 to 850, with 850 being the best possible credit score that you could receive, and 350 being the worst possible credit score.

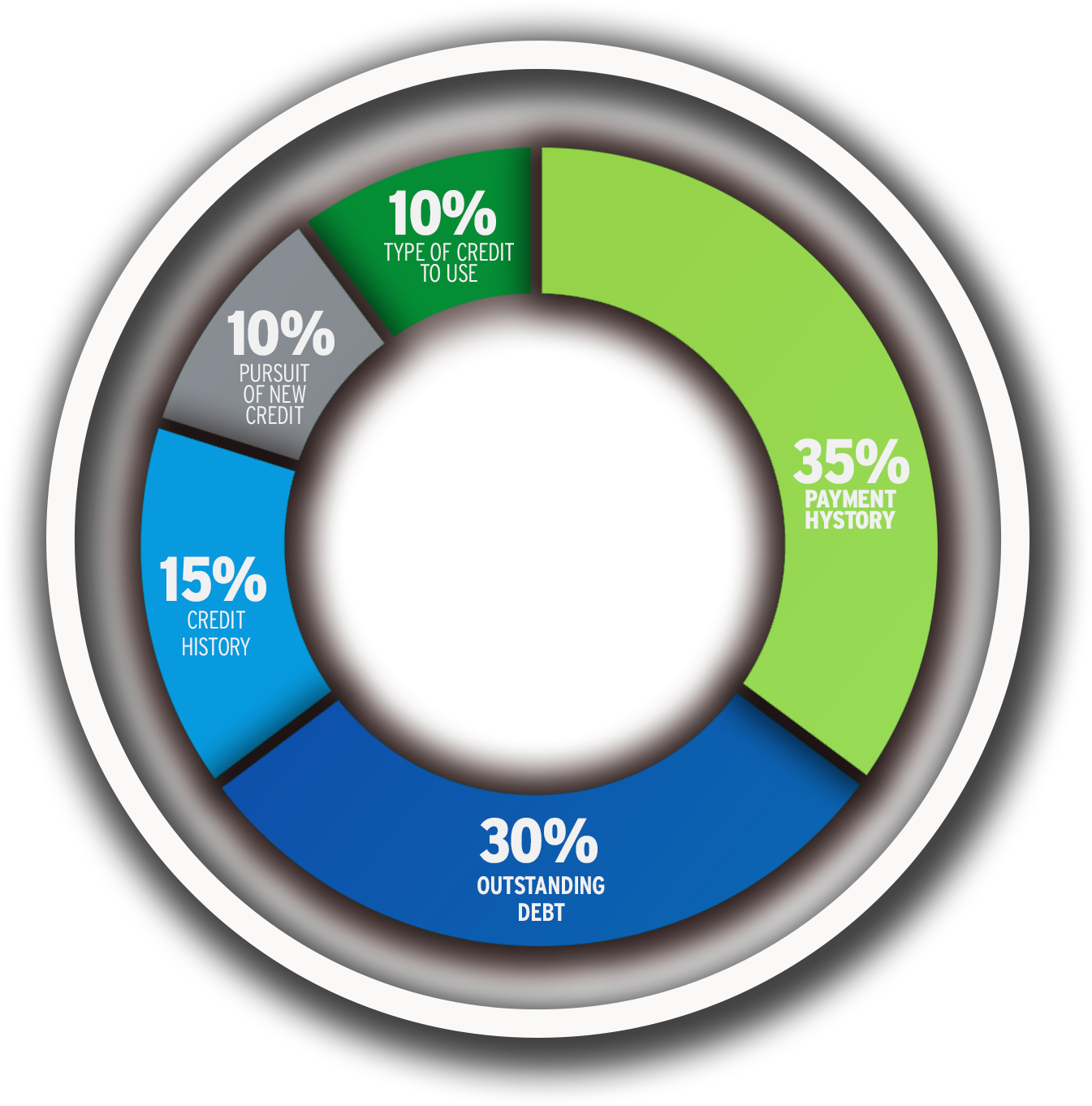

There are five factors that determine your credit score:

There are five factors that determine your credit score:

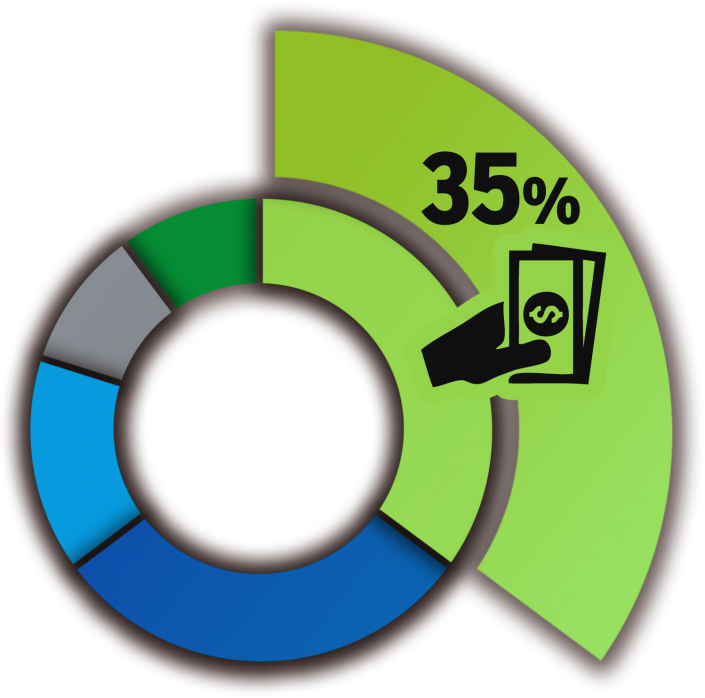

YOUR PAYMENT HISTORY

35% IMPACT ON YOUR CREDIT SCORE

Paying debt on time and in full has a positive impact. Late payments, judgments, charge-offs, collection accounts and bankruptcies have a negative impact.

Paying debt on time and in full has a positive impact. Late payments, judgments, charge-offs, collection accounts and bankruptcies have a negative impact.

If you have had any bankruptcies within the last 7 years, it will seriously affect your ability to borrow or establish new credit accounts.

If you have had any judgments within the last several years, it is very important that you pay off the judgment and get a “satisfaction of judgment” from the court.

Any unsatisfied or recent judgments will make a bad dent in your credit scores and adversely affect your ability to borrow. Usually, judgments and liens must be paid prior to the closing.

Timely mortgage payments are weighted heavily by the scoring systems and are one of the most vital requirements that lenders look for when evaluating your credit history. Many times a single late mortgage payment within the last 12 months can hold up your file or spell the difference between the best interest rate and the next credit level. Your payment history on other debts (car payments, credit cards, etc.) is also given a lot of weight.

The credit scoring systems evaluate how many late payments you have had and whether they were 30, 60 or 90 days late, or whether they are currently in default, with default being the worst situation.

Additionally the systems look at whether the late payments were consecutive. If you only have one or two minor late payments on your report with no other derogatory marks, your score will not be terribly affected, but you will have a tough time getting over the critical 700 level.

Here are four practical steps that you can implement to improve your credit score in the area of “Payments”:

✅ Make all your payments on time.

✅ Past dues on any account will destroy your score – bring your delinquent accounts current immediately.

✅ Pay your bills before they go to a collection agency

✅ Check your credit report for accuracy on a regular basis; and make sure that disputed bills are not negatively affecting your credit scores.

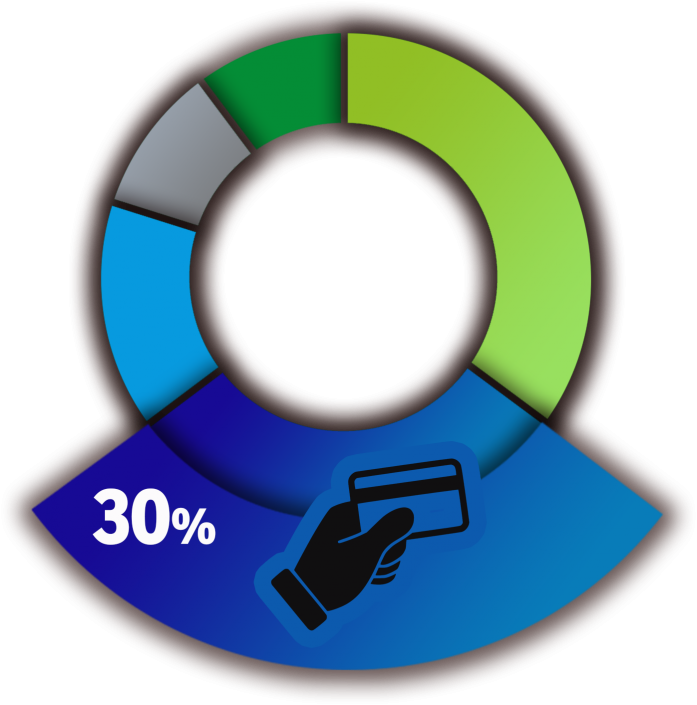

THE BALANCE YOU OWE VS. YOUR AVAILABLE CREDIT LINES

30% IMPACT ON YOUR CREDIT SCORE

Make all your payments on time. Past dues on any account will destroy your score – bring your delinquent accounts current immediately. Pay your bills before they Don’t close your credit accounts unless it is necessary to do so. It is better to have many open accounts with little or no balance than to have just one or two accounts regardless of the balance.

Make all your payments on time. Past dues on any account will destroy your score – bring your delinquent accounts current immediately. Pay your bills before they Don’t close your credit accounts unless it is necessary to do so. It is better to have many open accounts with little or no balance than to have just one or two accounts regardless of the balance.

Don’t concentrate large balances on just a few accounts.

Keeping your credit balances below 30% of your available limit is very important. Keeping your balances at 1-3% of your available credit is even better. For instance, if you owe $10,000, and you have $100,000 of credit available to you, you are only using 10% of your available credit line.

On the other hand, if you owe $10,000 and you only have $10,000 available to you, you have “maxed out” your available credit and your credit scores will be very negatively impacted. Therefore, it is not how much you owe, but how much you owe compared to what you are able to borrow.

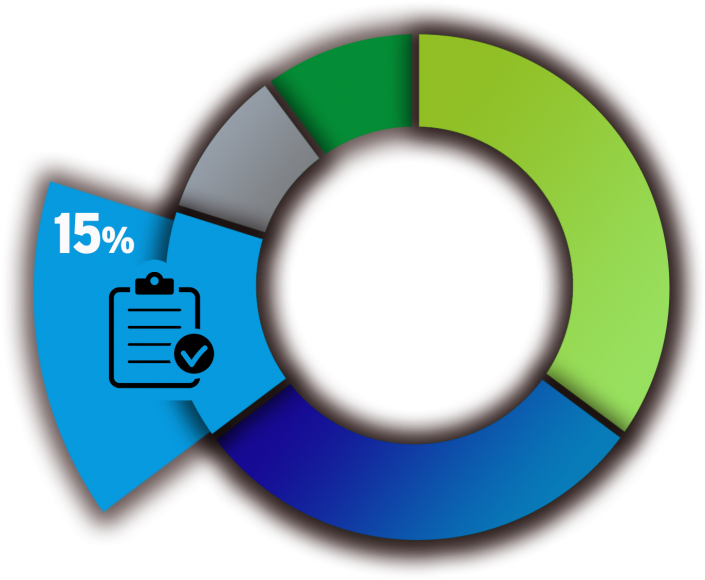

YOUR CREDIT HISTORY

(HOW LONG YOUR ACCOUNTS HAVE BEEN OPENED)

15% IMPACT ON YOUR SCORE

Don’t close your credit accounts. If you must, close the newest ones instead of the oldest ones.

Don’t close your credit accounts. If you must, close the newest ones instead of the oldest ones.

Your score will improve over time if you keep accounts open and use them every once in a while. Think twice before jumping on that latest 0% credit card offer or opening a new card just to get a 10% discount at a department store.

The longer your accounts have been opened, the higher your score will be; newly opened accounts will bring your score down. Here are three practical steps for you to improve your score in this area:-

✅ Think twice before jumping on that latest 0% credit card offer or opening a new card just to get a 10% discount at a department store.

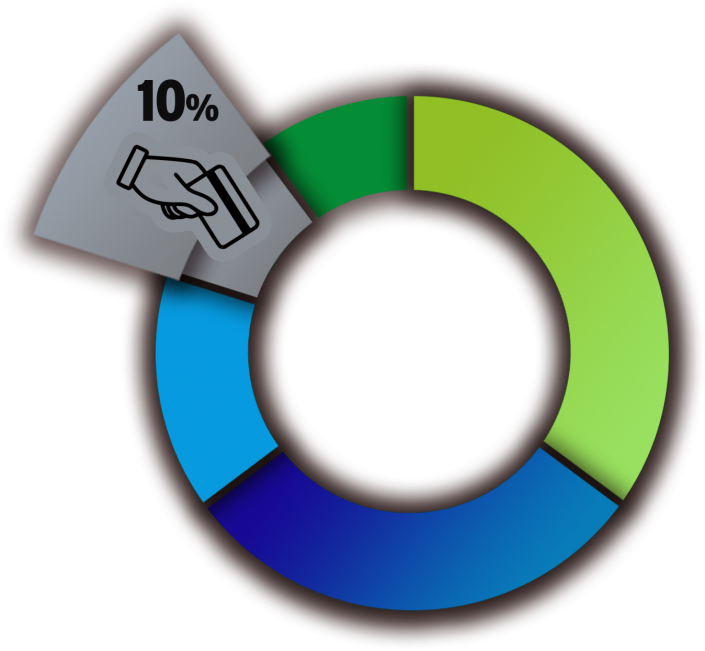

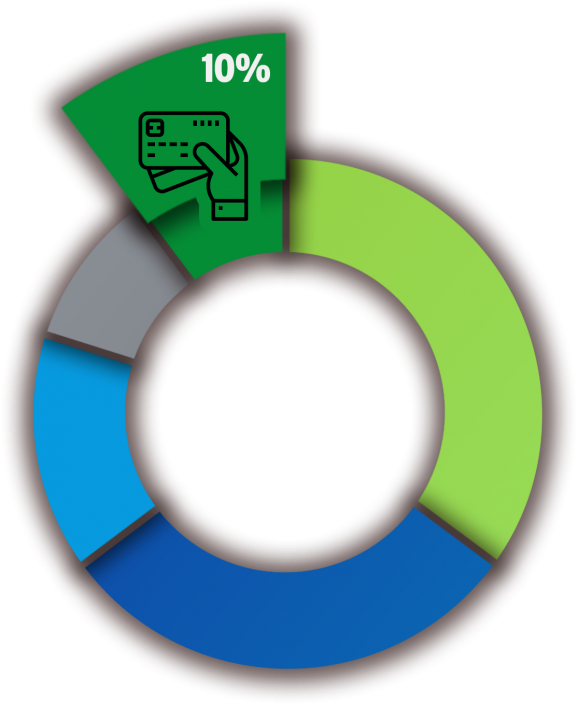

NUMBER OF RECENT INQUIRIES

MADE BY CREDITORS

10% IMPACT ON YOUR SCORE

Multiple auto and mortgage inquiries are treated as only one inquiry if made within 45 days of each other. So, it’s better to shop for a car or a mortgage over a two week time frame, rather than to prolong it over a longer time frame.

Multiple auto and mortgage inquiries are treated as only one inquiry if made within 45 days of each other. So, it’s better to shop for a car or a mortgage over a two week time frame, rather than to prolong it over a longer time frame.

Don’t apply for a lot of credit or open multiple credit cards at the same time; and If you’re thinking of applying for a mortgage within the next 90 days, it would be good to wait until after your loan closes before you apply for any new credit.

Inquiries affect the score for one year from the time they’re made. Your score isn’t impacted when you check your own report. It’s only affected if a potential creditor checks your credit. These include department stores, as well as credit card, auto finance and mortgage companies. Here are three steps you can take to improve your score in this area:

Having 3-5 revolving credit cards open is optimal; and, Having a good mix of auto loans, credit cards and mortgages is better than having only credit cards.

Having 3-5 revolving credit cards open is optimal; and, Having a good mix of auto loans, credit cards and mortgages is better than having only credit cards.